In early April, shortly after “Liberation Day,” the US bond vigilantes interrupted their month long vacation of what is normally a dull month just long enough to send a message to the markets and the White House.

Call me a skeptic on many things, but I do believe that Treasury Secretary Bessent and President Trump got the message, even if Omar Suarez the poor retail bagholder in the snapshot above wasn’t properly hedged for what was happening.

Fast forward to almost forty-five days later and let’s check the status of the trade war and how our President and his followers are dealing with the “negotiations” with China.

That doesn’t sound very much like a pro-capitalism approach to what and how tariffs impact the average American, especially since so many of his ardent followers shop there due to the economic deterioration which has occurred under the last four years of Jill Biden’s policies. I’m wagering the followers of President Trump decided to hold him to account for posts like this, right?

Never mind, it would appear the bond market is going to have to send another message. Despite the last message sent in early April, the administration’s short term memory is equal to that of those traders who buy memecoins and proclaim the next one named after a body function as the “future of finance” as today’s statements by Scott Bessent demonstrate.

Some argue that tariffs are a tax on the American people and will be inflationary. By that logic, cutting taxes should be deflationary.

— Treasury Secretary Scott Bessent (@SecScottBessent) May 18, 2025

Let’s pass @POTUS’ ONE BIG, BEAUTIFUL BILL, lower the burden on working families and businesses, and drive economic growth. pic.twitter.com/DKP2bArDl3

So on one side of the argument, Secretary Bessent fails to recognize or acknowledge that tariffs are indeed inflationary, as transition (sorry JayPo) costs are passed on to manufacturers and consumers for at least one or two quarters at a minimum. What is worse however is the obfuscation that the “big, beautiful tax bill” is some sort of major tax cut when as it is currently structured the legislation simply extends Biden era spending increases and programs while renewing the Trump tax program from 2018.

There is no major break for business, no income tax cuts for the middle class or working poor, and worse, no relief from increasing costs for numerous programs impacted by government overspending and regulations like Obamacare for example.

Naturally, this led to the big nothingburger news on Friday from Moody’s which the Secretary addressed in his interview on Meet the Press via NBC also, as reported by the Financial Times below:

Moody’s strips US of top-notch triple-A credit rating

Why is this a nothingburger?

Simple, the ratings action that Moody’s engaged in on Friday was blatantly political as it could have been done after the August 2022 enactment of the Inflation Reduction Act but as the ratings agencies enjoy doing, the “look at me” factor is more important than risking the wrath of a massive government regulatory authority under the Biden regime.

Whatever reaction the bond market engages in the upcoming days before the three day US holiday weekend is totally irrelevant to the downgrade even though that will be the excuse the mainstream financial media will attempt to promote to the ignorant public.

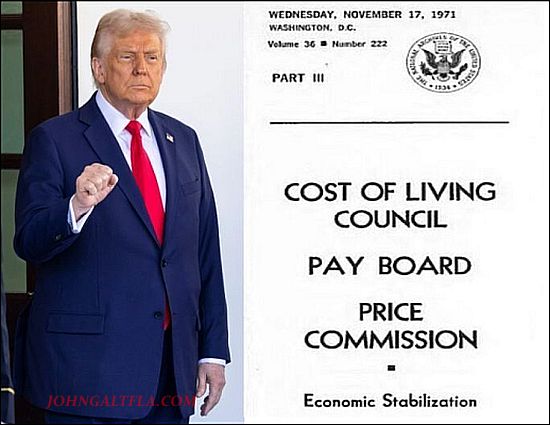

Is Trump on the Brink of Revisiting Nixon’s Policies?

On August 15, 1971 the Nixon Shock is mostly remembered for the US divorce from the gold standard and the Executive Orders directing the change in US policy regarding American gold reserves. However another Executive Order was issued that day which had implications as a direct assault on capitalism and had numerous individuals questioning Nixon’s conservative credentials.

Executive Order 11615—Providing for Stabilization of Prices, Rents, Wages, and Salaries

Excerpt:

WHEREAS, in order to stabilize the economy, reduce inflation, and minimize unemployment, it is necessary to stabilize prices, rents, wages, and salaries; and

WHEREAS, the present balance of payments situation makes it especially urgent to stabilize prices, rents, wages, and salaries in order to improve our competitive position in world trade and to protect the purchasing power of the dollar:

Now, THEREFORE, by virtue of the authority vested in me by the Constitution and statutes of the United States, including the Economic Stabilization Act of 1970 (P.L. 91-379, 84 Stat. 799), as amended, it is hereby ordered as follows:

SECTION 1. (a) Prices, rents, wages, and salaries shall be stabilized for a period of 90 days from the date hereof at levels not greater than the highest of those pertaining to a substantial volume of actual transactions by each individual, business, firm or other entity of any kind during the 30-day period ending August 14, 1971, for like or similar commodities or services. If no transactions occurred in that period, the ceiling will be the highest price, rent, salary or wage in the nearest preceding 30-day period in which transactions did occur. No person shall charge, assess, or receive, directly or indirectly in any transaction prices or rents in any form higher than those permitted hereunder, and no person shall, directly or indirectly, pay or agree to pay in any transaction wages or salaries in any form, or to use any means to obtain payment of wages and salaries in any form, higher than those permitted hereunder, whether by retroactive increase or otherwise.

(b) Each person engaged in the business of selling or providing commodities or services shall maintain available for public inspection a record of the highest prices or rents charged for such or similar commodities or services during the 30-day period ending August 14, 1971.

(c) The provisions of sections 1 and 2 hereof shall not apply to the prices charged for raw agricultural products.

SEC. 2. (a) There is hereby established the Cost of Living Council which shall act as an agency of the United States and which is hereinafter referred to as the Council.

I have added the emphasis to Section 2(a) for my readers because of who the individual was put in charge of the Cost of Living Council and how the twisted world of politics works:

If one thought it was Dick Cheney, that would be incorrect. It was the one and only Donald Rumsfeld who served as a member of Nixon’s economic team and illustrated that despite his business background, he was willing to step out of the bounds of American capitalism to impose theoretical policy solutions for inflation and soon stagflation.

The problem with historic events such as these in 1971 is that Trump is willing to issue Executive Orders in a similar fashion as Nixon to impose solutions which have a proven track record of failing and eventually creating pain for the American economy; pain far beyond the normal cycle of a recession or depression to remove the excesses and deadwood from the system.

Bessent: "I was on the phone with Doug McMillon, the CEO of Walmart, yesterday, and Walmart is in fact going to eat some of the tariffs." pic.twitter.com/kR0RnRkEMd

— Aaron Rupar (@atrupar) May 18, 2025

President Trump’s and Scott Bessent’s statements this weekend that despite the lack of an official proclamation or Executive Order stating such, the concept of imposing price controls on companies and markets is not that far fetched, especially after President Trump’s action against the pharmaceutical industry.

The Bond Vigilantes Might be Warming up their Helicopters Again

The recent stormy road in equities has been forgotten to what appears to be a similar to 2001 or 2007 bear market dead cat bounce and the short term reduction in bond yields. Despite repeated incidents of Asian Treasury Bill overnight liquidations, most likely Japanese banks and/or insurers, the relative stability has empowered the equity bulls to ignore the bond market warnings from April. For lack of a better term, they have decided to “act the fool” under the misconception that the trade war is over and China will simply fall into line like the United Kingdom.

Even Barron’s has recently warned about the mistakes that this and other administrations have made regarding the evaluation of inflation in their May 7th article:

We’ve Been Wrong About Inflation for Years. Fixing It Now Requires New Thinking

This one excerpt highlight just how far behind the curve US and in many cases, global central banks and policy makers might well be:

The low-inflation world appears to have been replaced by a new era of sustained inflation. Part of our collective surprise at this shift stems from a blinkered understanding of inflation itself. Economists overlearned the lessons of the last great era of inflation, leaving us with too few tools to respond when the problem returned. Hopes that the Federal Reserve and other central banks can quash the problem by simply raising interest rates are likely to be dashed.

There is good reason to believe that the old inflation regime won’t quickly return. First, as former U.K. central banker Charles Goodhart and others have observed, the deflationary forces that pushed prices down globally over the past 30 years are dissipating. That period saw a half-billion Chinese workers join the global labor pool, supply chains extend worldwide, and a broad acceptance of immigration. But those one-shot gains are unlikely to be repeated. Now, geopolitical competition is intensifying. States are attempting to claw manufacturing back home.

The emphasis is my own of course but highlights the risks of misjudging the current economic environment and presuming the history of anti-inflationary policies along with using past performance of protectionism with higher tariff policies will indeed allow for price stability in concert with economic growth.

This is why I advocate for the short and intermediate term to ignore equities and speculative financial instruments for evaluating economic projections while moving one’s focus to credit markets of all types as this administration engages deeper into the trade war. Unless one is a nimble short term trader or speculator, these markets are fraught with danger for the uninitiated app driven soul.

Historically, errors of judgment have consequences, and the US bond market has a tendency to highlight how there could be a boomerang effect against the irrational exuberance expressed in the past four weeks.

The Bank of America ICE Move Index indicator for US Treasury bond volatility looks stable enough although it has been trading almost since its inception at a higher level indicative of long term instability. If the pattern holds, especially after all of the news last week and this weekend, the reversal to the upside should occur again and any breakout above the 127 level is extremely bearish for bonds and equities.

The TLT is also making noise and thus worthy of watching next week for the same reasons:

The lack of a long term trend change to get the price back above the 100 level since 2023 is still extremely bearish for the intermediate and long term in this author’s opinion. By reviewing the longer term weekly chart, a disturbing pattern emerges which unfortunately for the administration coincides with some of their poor policy pronouncements and actions of the past several weeks.

Ever since Trump v1.0 and Biden chose a massive fiscal inflationary policy post-pandemic era, the TLT and US Treasury markets have been warning about the lack of serious efforts to withdraw the stimulus of that era or contract the size of government. This unfortunate fact seems to indicate that a retest of the 2023 lows might well be in the near future which would have massive impacts not only on US Treasuries, but impact corporate and speculative bonds in an adverse manner.

Asia Opens With a Sunday Night Court Judgment on US Bonds

On the initial open, there was a waterfall in US equity futures as expected but not worthy of focus for the moment.

The US bond futures are now trading along with Tokyo opening and just after 8 pm tonight, the move has been somewhat muted(data via CNBC.com):

Bitcoin once again demonstrates it is part of the future ABD (Anything but Dollars) trade:

And of course, gold starts the week on fire again as the Asian market continues it’s flight to safety:

Stay tuned as this could be one wild week in markets as the trade war nightmare gets more interesting.