99% of all the idiots one hears on television, radio, or the internet NEVER read the 8K financial report for any company. I am not singling out one website, one company, or one network, nor FinTwit media; I am trying to make a point. People NEVER read the facts and always skip to the highlights because they are lazy.

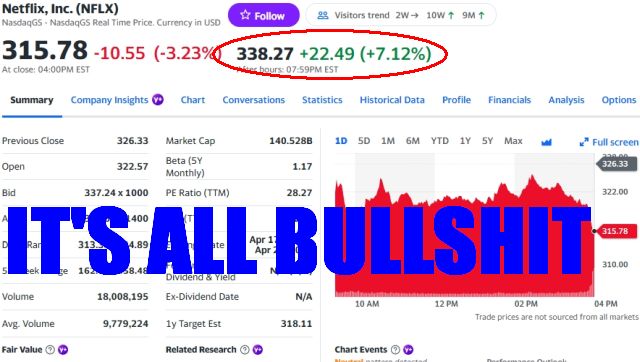

NetFlix reported “better than expected results” because they used incentives to dilute their bottom line and add suckers, er, subscribers to their network. The reality is that it cost them a lot of 2022’s positive gains because people took advantage of the “freebies” to stream and will soon quit NetFlix in favor of cheaper streaming options for the long term because cable television has turned into the whorehouse of the damned monopoly many of us were worried about.

For example, I’m not picking on ZeroHedge, hell they break it down better than most almost all of the time but sometimes they just cherry pick the headlines from the FT or WSJ. Tonight is now different from their thread:

Netflix Surges After Sub Growth Smashes Expectations, Resumes Buybacks, Hastings Steps Down As CEO

The very selected highlights from ZH via the shareholder letter which highlights the lowlights and hopium:

So with all that in mind, here are the details from the fourth quarter letter with news hitting moments before the results that CEO Reed Hastings is stepping down as CEO:

- Q3 Revenue $7.85 billion, +1.9% y/y, in line with the estimate $7.86 billion

- Q3 EPS 12c vs. $1.33 y/y, missing the estimate 42c

But while the financials were ok, it was the blowout number of subscriber adds that blew away expectations, and that everyone is focusing on:

- Streaming paid net change +7.66 million, down modestly -7.5% y/y, but smashing the estimate +4.5 million

- UCAN streaming paid net change +910,000, -24% y/y, beating the estimate +553,653

- EMEA streaming paid net change +3.20 million, -9.6% y/y, beating the estimate +1.3 million

- LATAM streaming paid net change +1.76 million, +81% y/y, beating the estimate +727,190

- APAC streaming paid net change +1.80 million, -30% y/y, beating the estimate +1.9 million

- Streaming paid memberships 230.75 million, +4% y/y, beating the estimate 227.3 million

- Operating margin 7% vs. 8.2% y/y, beating the estimate 4.45%

- Operating income $550 million, -13% y/y, beating the estimate $393.2 million

- Free cash flow $332 million vs. negative $569 million y/y, below the estimate of negative $199.2 million

Blah, blah, blah.

There is only one number that matters that the media, Wall Street, CNBS, FBN, and Bloomberg will NEVER focus on:

Margin.

As someone who ran larger transportation operations company and manufacturing operation which was 100% dependent on operating margin (cost me dearly at a 1.22%, trust me), margin in high volume consumer based businesses is all that mattes. So what did Netflix say from their very own 8K:

So basically a 7% operating margin is “okay” if one is expanding reach despite destroying net revenue and profitability growth. That used to be corporate suicide. Add in the diluted EPS (which CNBS, etc. ignores) and year over year growth and this is company heading into the Comcast or Viacom stagnant growth graveyard.

But wait, there’s more:

Woah. Wut?

“A clear path to reaccelerate our revenue growth“is the kind of statement that I read 22 years ago.

From AOL.

Or Netscape.

Hell, even Pets.com had those optimistic statements.

Folks, quit listening to “just” the headlines. Do not invest on faith, cults, arseholes yelling at you with plastic animals on CNBS, or anything the business propaganda channels throw at you.

Read the God Damned reports.

Then make decisions with your money.

Jamie Dimon told you to do that, but most do not listen.

And that dude runs the anchor bank for the Federal Reserve.